The MLI saga: Few more legislative blind spots?

The landmark ruling in the case of Sky High Appeal XLIII Leasing Company Limited has attained significant attention. The Hon’ble Tribunal held that the Multilateral Instrument (MLI), even though notified generally vide Notification No. 57 of 2019, cannot be effective unless a separate notification is issued to make the MLI amendments effective qua a particular Covered Tax Agreement (CTA). The Tribunal relied upon the Hon’ble Supreme Court’s decision in Nestle SA.

Revenue’s primary defence before the Tribunal was that MLI does not amend the text of the CTA; instead, it is applied alongside the tax treaties, modifying their application. Accordingly, it was contended the Notification No. 57 of 2019 was sufficient.

This contention of the Revenue was emphatically rejected by the Tribunal, holding that since Revenue admits that MLI modifies tax treaties, it cannot sidestep the legal requirement of issuing a separate notification u/s 90 for incorporating the modifications into domestic law, as held in Nestle SA.

Beyond this case, there appear to be other legislative misfires that may render the MLI a dead letter:

𝗮) Plain language of section 90 per se does not grant any sanctity to any standalone multilateral instrument. Hence, MLI as a separate instrument may not have any effect unless MLI modifications are made in the CTAs (and notified separately).

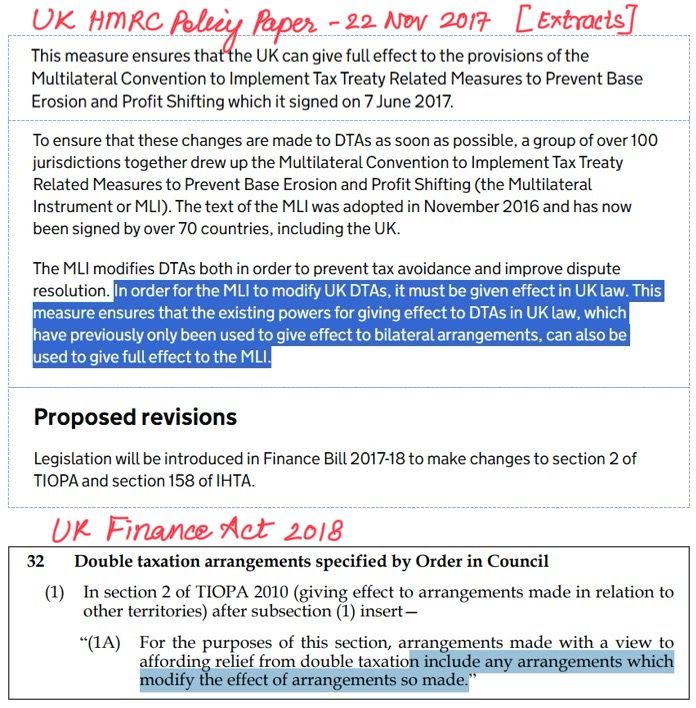

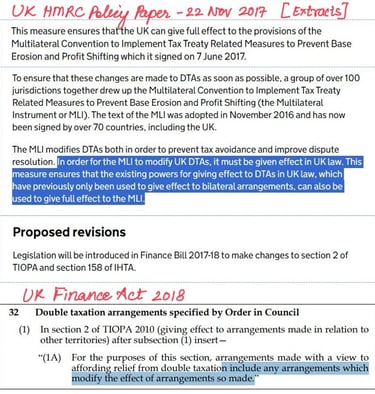

In this regard, a parallel may be drawn from the UK tax laws. Section 2 of the TIOP Act 2010 (𝘴𝘪𝘮𝘪𝘭𝘢𝘳 𝘵𝘰 𝘴𝘦𝘤𝘵𝘪𝘰𝘯 90) only allowed for entering into bilateral tax treaties. In order to implement MLI, it was specifically amended to enable Her Majesty to enter into “arrangements which modify the effect of arrangements so made”.

Interestingly, no such amendment has been made u/s 90.

𝗯) Further, the validity of the Notification No. 57 of 2019 issued u/s 90 is also liable to be challenged for more reasons than one.

For instance, Section 90(1)(b) originally empowered the Govt only to enter into agreements for avoidance of double taxation. It was amended vide the Finance Act 2020, w.e.f. 1.4.2021, with a view to enable the Govt to include the MLI preamble in the CTAs (as explicitly stated in the Memorandum to the Finance Bill 2020). This implies that even the power to include the MLI preamble was absent u/s 90 prior to 1.4.2021. If so, how could a Notification be issued u/s 90 in 2019 to implement the MLI?

Sky High may seem to complete the Nestle SA loop, putting the Revenue in a catch-22. But it’s not just a loop; it’s a hyperloop set to witness “multilateral” litigation.

Citation: [TS-1085-ITAT-2025(Mum)]