Can Crypto losses be set off against Crypto gains?

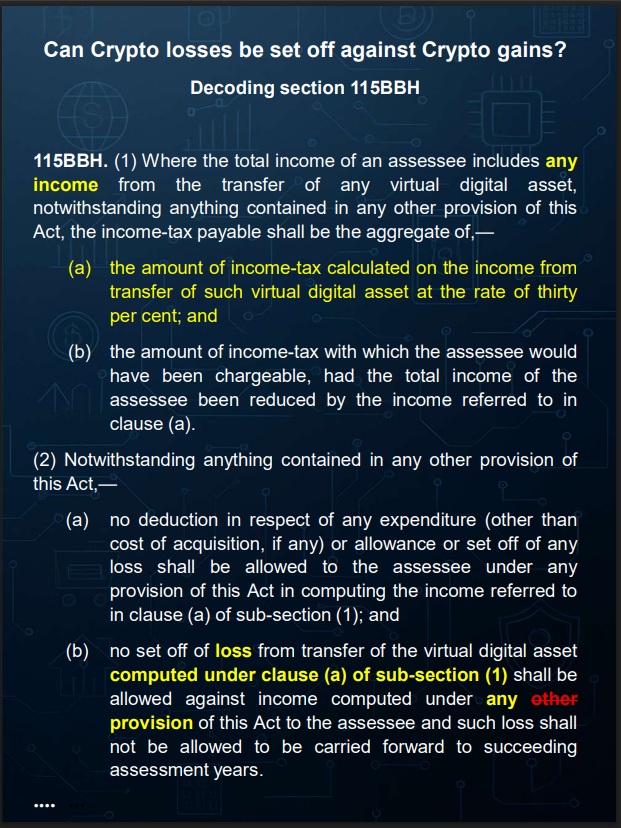

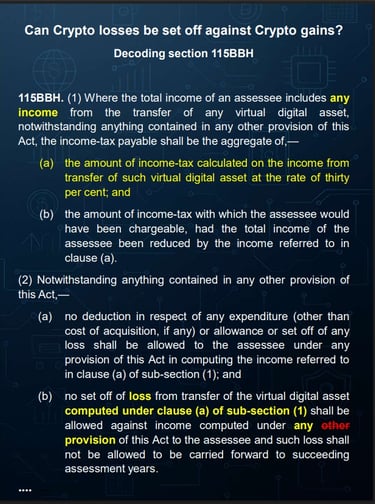

Section 115BBH, introduced vide the Finance Act 2022, provides for a separate scheme for taxing income from transfer of Virtual Digital Assets (VDAs) at 30%.

Earlier, the Finance Bill 2022 and its Memorandum had stated that VDA losses cannot be set off against income under “any other provision” of the Act, meaning thereby that such losses could be set off against VDA gains.

However, the word 'other' was omitted in the enacted law.

This has led to a widespread interpretation that VDA losses cannot be set off even against VDA gains.

Illustratively, if one earns ₹2 lakh on Bitcoin and loses ₹1 lakh on Altcoin, the loss is ignored ('dead loss') and full ₹2 lakh is taxed at 30%. Even the ITR forms have been designed on this basis.

Alternative view:

Interestingly, section 115BBH(2)(b) restricts set-off of “loss computed under clause (a) of sub-section (1).” However, clause (a) of sub-section (1) only speaks of 'income'. Why would the law provide for computation of 'loss' under a provision that only refers to 'income'?

A logical inference would be that the word ‘income’ would naturally include ‘loss’, which is a settled legal position. If that be so, computation under section 115BBH(1)(a) would have to include trades resulting in income as well as loss, i.e., it cannot be restricted to only positive trades.

Even otherwise, if 115BBH(1)(a) were to apply only to positive trades, there would never be an occasion where any ‘loss’ would arise under this clause. In such a scenario, section 115BBH(2)(b), which specifically refers to 'loss computed under section 115BBH(1)(a)', would be rendered otiose and redundant.

It is settled law that an interpretation which renders a provision ineffective is to be ignored. Thus, to give full effect, it could be argued that section 115BBH should be read harmoniously as under:

a) computation under 115BBH(1)(a) would be the ‘net amount’, which would inherently involve ‘netting’ off (not ‘setting’ off) VDA losses against VDA gains during the year;

b) if there is net gain, it is to be taxed at 30% u/s 115BBH(1)(a);

c) if there is net loss, it would be dead loss u/s 115BBH(2)(b).

Thus, it could be argued that dropping of the word ‘other’ in the FA 2022 does not make any difference and the original intent to allow netting off remains intact.

In any case, if two interpretations are possible, shouldn’t the one aligned with the original legislative intent, logic, and the real income theory prevail?

After all, when speculation losses and even Crypto F&O losses are allowed to be set off against respective gains, why should crypto be treated differently? That too in absence of any express legislative intent for doing so?

#115BBH #CryptoTax #loss #TaxLitigation