Bombay HC's decision on section 50C and leasehold land: Unintended consequences

Section 50C is triggered when a ‘capital asset, being land or building or both’ is transferred for consideration lower than the stamp duty value.

Recently, in Vidarbha Veneer Industries Ltd. (ITA 34/2022), the Hon'ble Bombay HC (Nagpur Bench) has held that section 50C applies even to transfer of leasehold rights in land. The Court reasoned:

• A '𝘤𝘢𝘱𝘪𝘵𝘢𝘭 𝘢𝘴𝘴𝘦𝘵' u/s 2(14) includes property of any kind ‘held’ by an assessee - not necessarily ‘owned’. Thus, land or building could be 'held' as an owner, lessee, sub-lessee, “tenant” etc.

• The word '𝘵𝘳𝘢𝘯𝘴𝘧𝘦𝘳' under section 50C will have widest amplitude covering all modes of transfer.

Read literally, this decision may lead to unintended consequences and could trigger 50C even in cases of normal tenancy - since a rented apartment may be treated as the tenant’s ‘capital asset’ and the expiry of the tenancy as a ‘transfer’, being 'extinguishment' of the tenancy right.

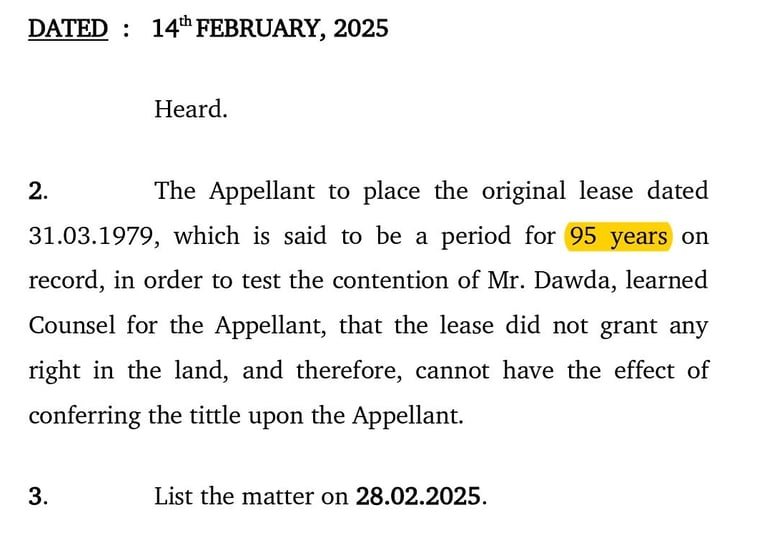

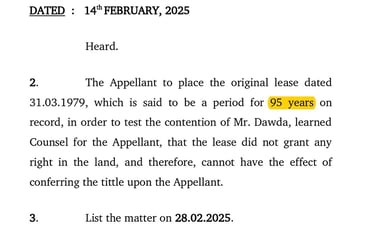

It is a settled principle that the ratio of a judgement has to be read in light of the underlying facts. While this judgement does not discuss the terms/duration of lease, an interim order in the same case notes that it was a lease for 95 years, generally referred to as a perpetual lease.

Thus, to distinguish this decision’s applicability in appropriate cases, it would be crucial to read the judgement along with the interim order.

On a separate note, there are two core arguments against the applicability of section 50C qua leasehold land, basis which Tribunal benches had been taking a view in favour of taxpayers, viz;

• The legislature distinguishes between ‘land or building’ and ‘rights therein’ (ref: section 54D) - However, section 50C doesn’t refer to any such 'rights';

• 50C being a deeming fiction has to be read strictly – its scope cannot be extended beyond the intended purpose.

Additionally, the Memo to FB 2002 itself states the intention of the legislature that 50C would apply to 'transfer of immovable property'. Thus, there may not be any need at all to interpose the definition of a 'capital asset' u/s 2(14) for interpreting section 50C.

Since these arguments were not dealt in the judgement, they do offer a hope for a different conclusion as the jurisprudence evolves.

Till then, what could be the other unintended consequences?

Link: https://lnkd.in/dEd8-TFu

#taxlitigation #BombayHC